Tokenizing Trillions: Key Gaps and Strategies

We are at the early stages of a new financial era. Tokenization is no longer a niche experiment. It is rapidly becoming a serious arena in which institutions compete to lead one of the largest new asset categories and where capital allocators pursue meaningfully better returns.

The question is no longer whether trillions will move onchain, but who will lead it. This piece examines what it will take to reach escape velocity — and the opportunities for operators and entrepreneurs to build the platforms on which trillions are custodied and traded.

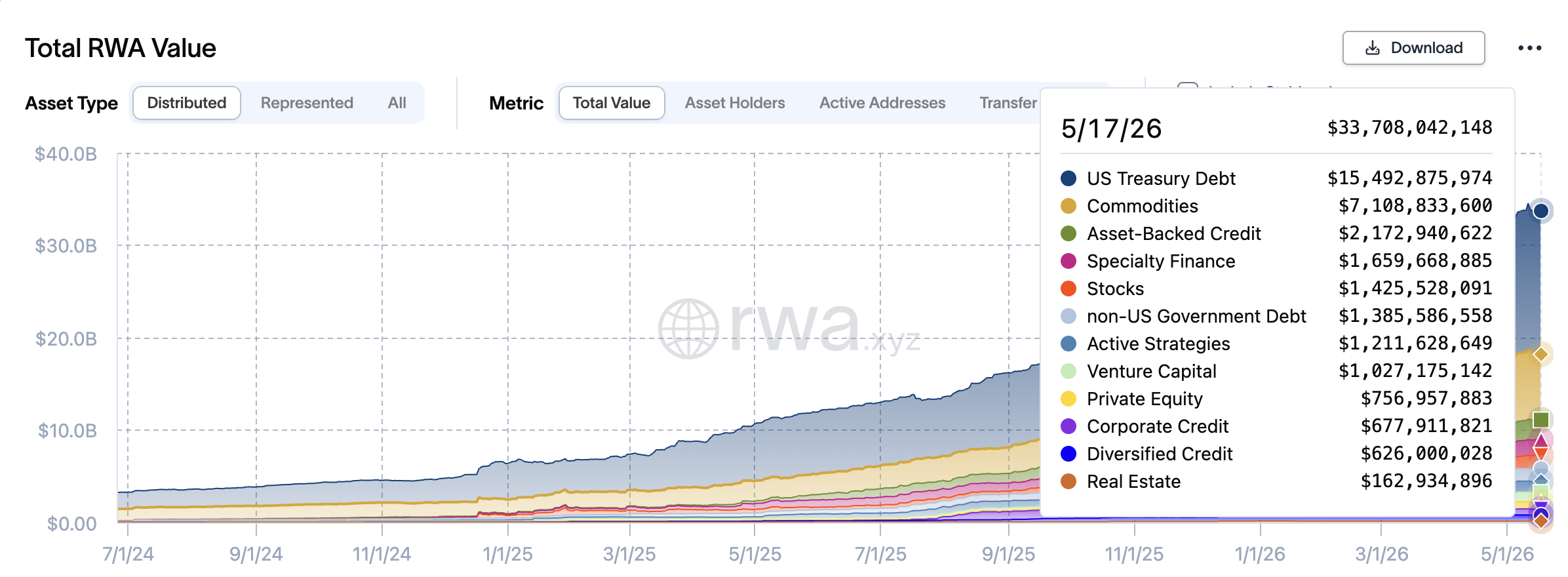

Tokenized finance has already reached a meaningful scale. Stablecoins alone now exceed $320 billion in circulation, while other tokenized financial assets represent more than $30 billion across products including money market funds, private credit, equities, commodities, and more. Many of the world’s largest asset managers — including BlackRock, Fidelity, and Franklin Templeton — have collectively brought billions of dollars of real-world assets onchain.

Fig 1: Tokenized Financial Assets (excl. stablecoins) — rwa.xyz

While crypto has performed well as a nascent industry, scaling tokenized finance to trillions will require meaningful advances in both technology and institutional-grade risk management.

It’s All About Risk-Adjusted Returns

The growth of Tokenized Finance is contingent on delivering superior risk-adjusted returns relative to traditional finance, otherwise assets will remain offchain. Tokenizing an asset must improve capital deployment through better returns, lower units of risk, and/or meaningful operational and capital efficiency advantages over existing financial infrastructure.

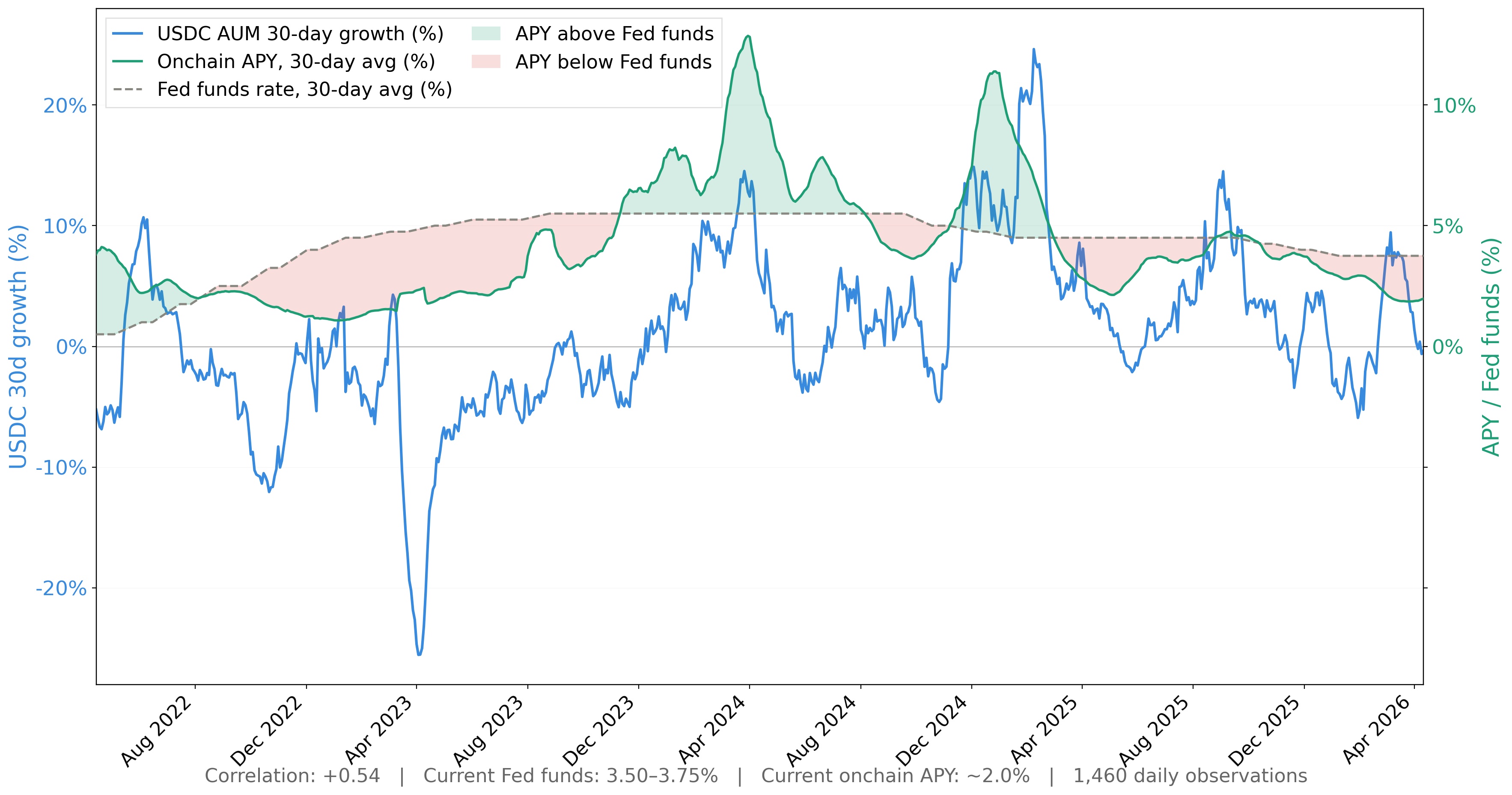

Historical stablecoin flows show the importance of risk-adjusted returns clearly. AUM grew fastest when on-chain “risk-free” yields (proxied by Aave USDC) materially exceeded the Federal Funds rate, from late 2023 through August 2024. It contracted when on-chain yields fell below the Fed Funds rate in 2022–2023. Stablecoins initially came onchain for many reasons — trading, transfers, and dollar access — not just yield. But when on-chain yields became unattractive relative to traditional options, capital left.

This pattern — capital flowing toward superior risk-adjusted returns — is not isolated to stablecoins. It reflects a broader historical progression in how tokenized finance has developed, and where it is headed next.

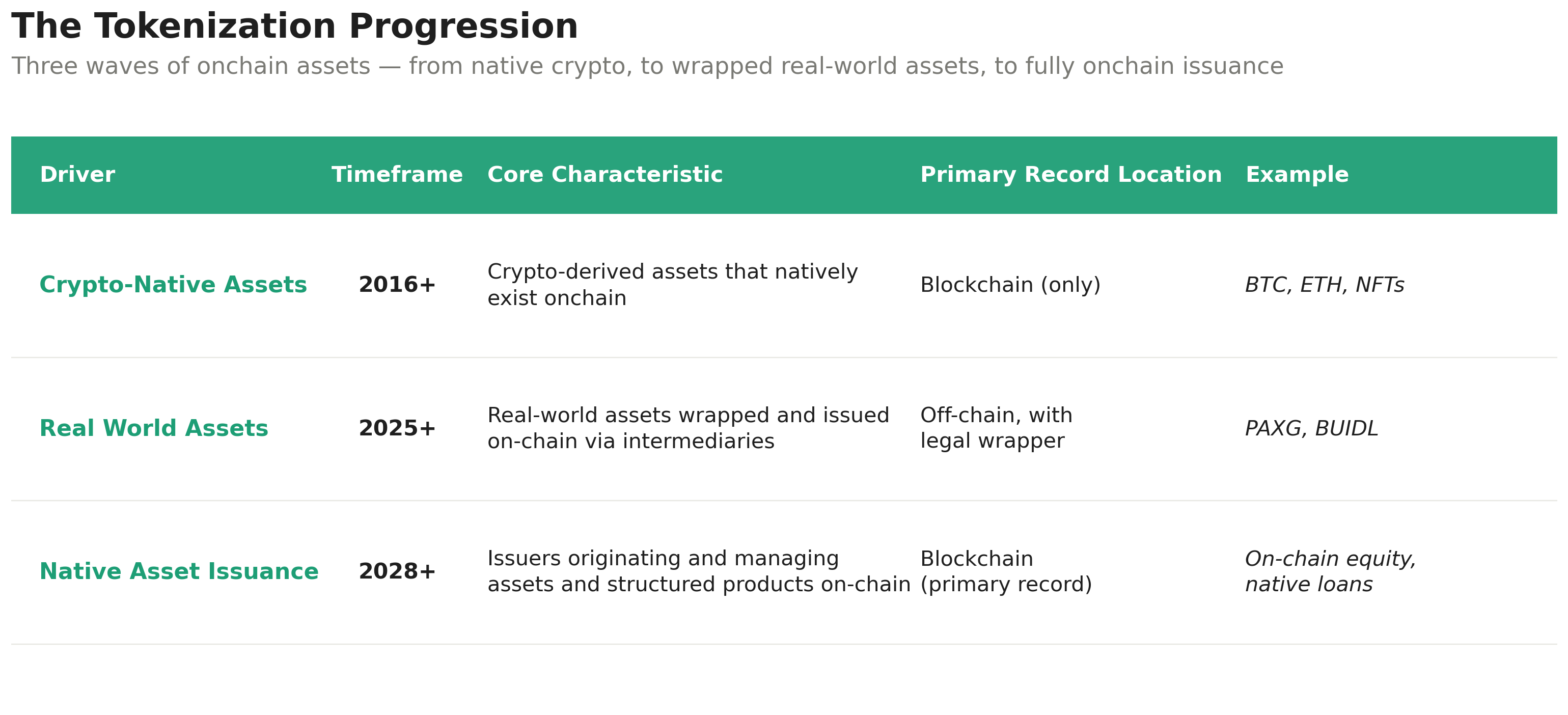

The Tokenization Progression

What began as tokenizing dollars to trade crypto-native assets has since expanded to include real-world assets, with native on-chain issuance emerging as the next major driver.

Tokenization started with users wanting to trade crypto-native assets such as cryptocurrencies and NFTs. Stablecoins emerged as a practical medium to transfer value across exchanges, quote prices in dollars, and store value on-chain.

Real World Assets (RWAs) became a meaningful driver starting in 2025. These are traditional financial assets — such as money market funds, private credit, and equities — that are wrapped and issued on-chain by intermediaries. The tokens function similarly to ‘warehouse receipts’ – digital claims – on the underlying assets. However, the primary source of record remains off-chain, and an additional legal structure is required to connect token holders to the real asset. This downstream approach improves accessibility but also introduces dual administration and extra counterparty risk.

A longer-term goal is Native Asset Issuance, where origination and issuance happen directly on-chain. Examples include native on-chain lending and blockchain-based equity issuance. When blockchain is built into financial operations from the start, it can improve capital efficiency through better yields, lower operational costs, faster capital recycling, and greater transparency. The first meaningful wave of native issuance will likely come from new companies building PayFi and credit infrastructure rather than legacy institutions.

We should expect these different models to coexist for a long time. The current phase is about proving product-market fit and building deep, reliable liquidity. Only once the AUM becomes meaningful will institutions start treating blockchains as a primary venue rather than a secondary one.

Therefore it’s helpful to identify the assets and use cases where tokenization can demonstrably reach trillions, and move it from a “nice to have” for institutions to a core strategic mandate.

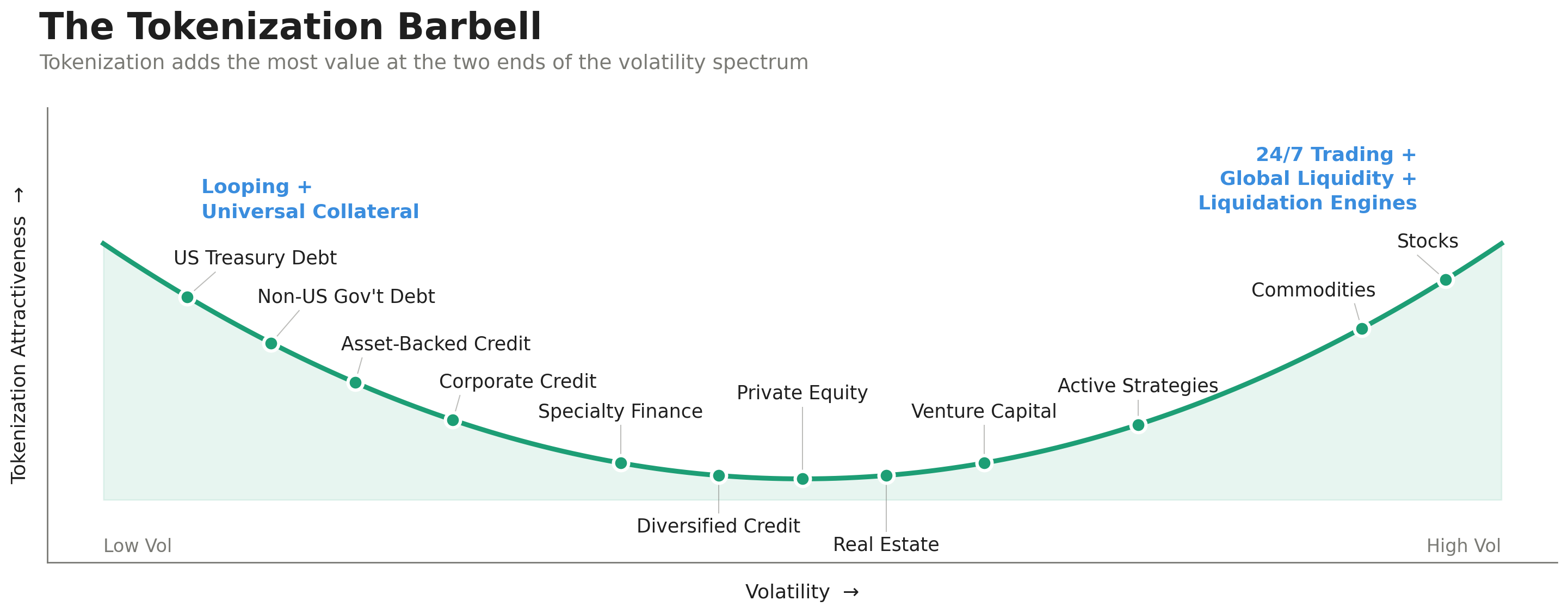

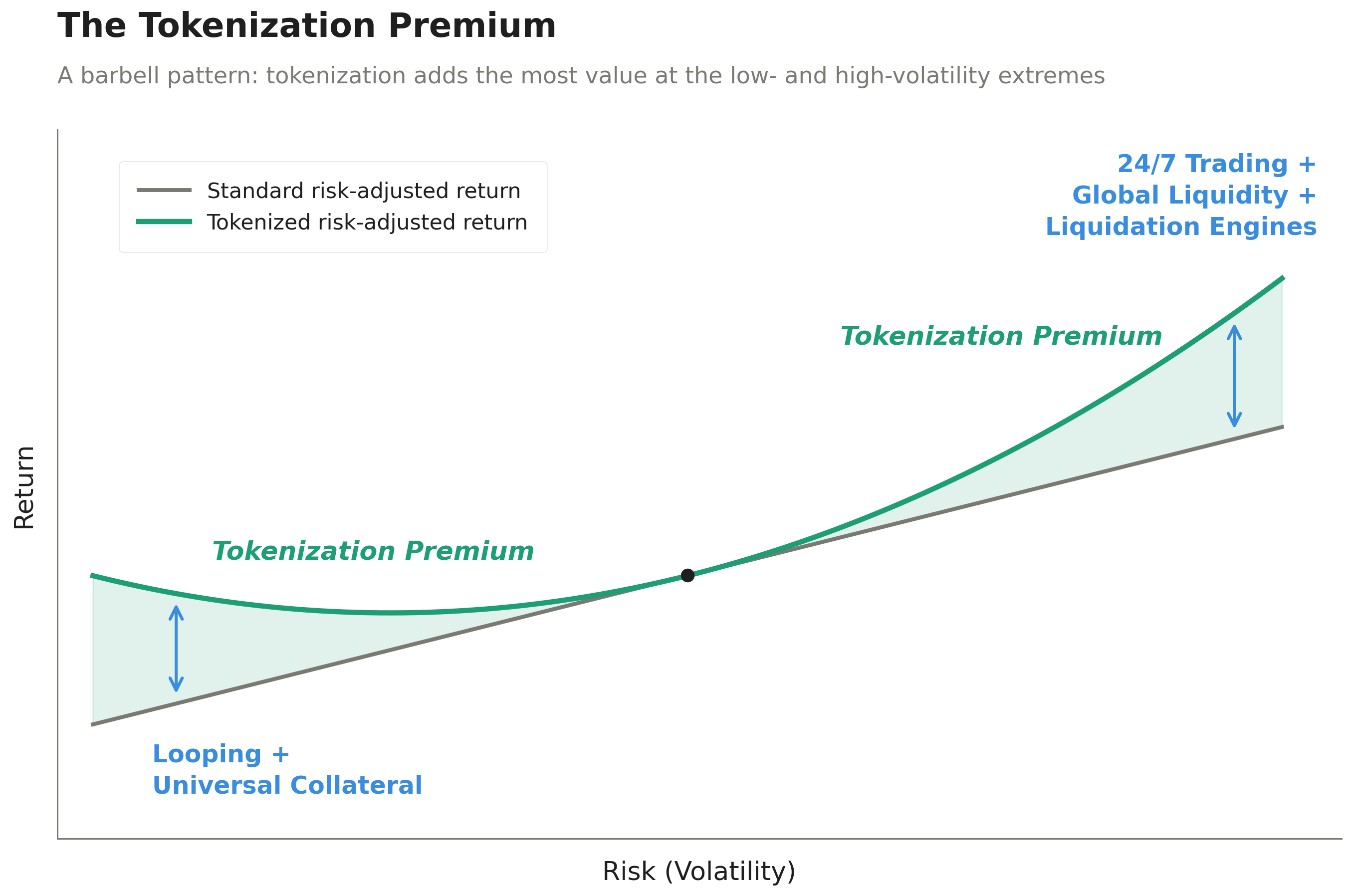

The Tokenization Premium

Because tokenized finance must ultimately deliver superior risk-adjusted returns, the practical question becomes: where and how? Which assets should issuers and allocators prioritize?

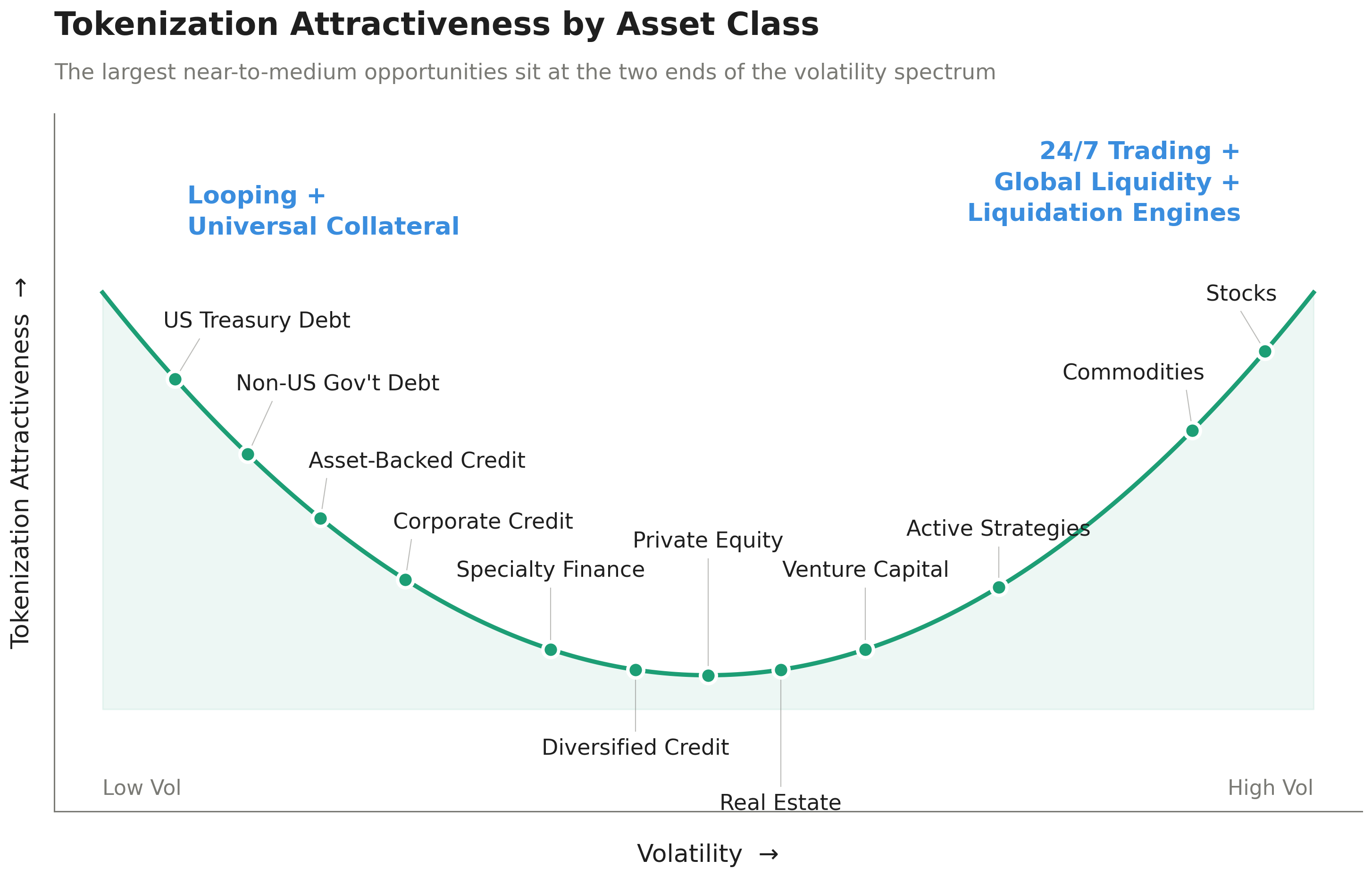

It is useful to think from first principles. I propose the Tokenization Premium as a framework for identifying where tokenization creates the greatest value. The benefits are not evenly distributed. They follow a barbell pattern — the clearest and most powerful advantages appear at the two extremes: very low-volatility assets and very high-volatility assets.

Low-volatility assets are clear near-term winners. Assets like tokenized Stretch (STRC) and money market funds (e.g., BlackRock’s BUIDL) deliver steady, predictable yields that can be looped, used as collateral, or deployed in durable yield strategies at multiples that are difficult or impossible in traditional finance. These assets are ideal for institutional capital that prioritizes yield-bearing collateral for basis-trading and companies looking to keep capital onchain. Tokenization turns them into composable, 24/7 collateral that can be looped and used across protocols with minimal friction — creating a structural advantage over off-chain equivalents.

High-volatility assets benefit from an entirely different set of advantages. Crypto-native assets (BTC, ETH, SOL), on-chain derivatives (perpetuals, structured products like Ethena), and tokenized stocks and commodities benefit 24/7 global trading, permissionless and orderly liquidations, real-time price discovery via robust oracles, and deep composability. Risk-on positions can be entered and exited instantly, without delay, and new trading experiences, indices, and structured products can be built that simply aren’t possible with quarterly NAVs or traditional settlement cycles. These assets thrive in an environment where speed, transparency, and atomic composability matter most.

Assets trapped in the messy middle — moderate volatility with moderate yields — struggle in the current Real World Asset era. They rarely generate enough yield to justify heavy looping without liquidation risk, and they cannot fully leverage 24/7 trading due to infrequent oracle updates or manual processes. While solutions like Upshift’s Clear exist to enable immediate settlement, this category is unlikely to be the primary near-term driver of growth.

Applying the framework to asset classes illustrates where the largest near-to-medium opportunities are:

The Tokenization Premium isn’t exhaustive and doesn’t cover less important considerations like whether the asset is publicly vs privately traded, counterparty risk, and the liquidity profile of the asset. But from first principles it provides a structural reference point that best leverages the benefits of tokenization.

Even for the assets that should be tokenized, at least three barriers prevent capital from moving onchain at scale.

1/ Investors Need Better Security Guarantees

Modern Portfolio Theory defines risk as volatility. Tokenized assets carry two more: protocol risk and liquidity risk.

In the early years of DeFi hacks were routine – or at least not surprising. Most of them were smart contract related, and after each one developers dutifully upgraded their smart contracts to ensure that across the ecosystem, it could never happen again. After that era, starting around 2024, many believed large-scale, nine-figure hacks wouldn’t happen again. They were partially right.

Fast forward and the hacks continue and are increasingly sophisticated. The current wave is OpSec related, with Drift and KelpDAO alone exceeding $500m in losses this year [link, link]. Even large, sophisticated, centralized companies like ByBit were hacked for $1.5b as recently as 2025 [link].

What’s clear is this is an endless game of cat and mouse, and the properties that make crypto and blockchains superior financial assets – instantaneous settlement and permissionlessness – render a challenge to make them 100% secure.

However, the cat now has tools more powerful than the world has ever seen; the next generation of AI models. Anthropic’s Mythos model is ostensibly so advanced that it’s found security vulnerabilities in the most foundational platforms like Linux, Apple and more. Hackers like the Lazarus group of North Korea can use these to accelerate the rate of security exploits, even when developers use it as a Blue team ally.

The current approach to on-chain security is no longer sufficient. Institutions will not commit trillions to systems in which a single exploit can still drain hundreds of millions in a matter of moments.

What is required now is a Security Renaissance — a deliberate and disciplined rethinking of how we design, govern, and establish trust in on-chain finance. This will demand both common-sense improvements and new primitives. Protocols and companies that innovate will earn the confidence of serious capital. Those that do not will struggle to attract it.

On-chain finance would benefit from greater institutional-grade discipline around security architecture. The first and most obvious actions are implementing standards around multi-sig design, withdrawal limits & time locks, upgrade authorities, and transparency around security architecture. I was honestly stunned when I saw that Drift relied on a 2-of-5 multisig with no timelocks. Similarly, when KelpDAO had a single DVN (i.e. signer) for its bridge smart contracts.

I’m excited for a new standard of transparency reports and certifications which create a clear baseline for institutional participation. Protocols that lead with transparency and robust design will be rewarded with greater capital flows; institutions have deep risk departments and require robust protections. It’s impossible to catch every bug, so instead teams that implement common sense circuit breakers and more robust upgrade processes will be more attractive to issuers, institutions and retail.

Second, teams should consider issuing their own stablecoin. This offers dual benefits; provides revenue to the protocol and provides an immediate freeze and seize capability. The first moments during an attack are the most critical, and the ability to act quickly and unilaterally is critical. Why not rely on existing stablecoin issuers to immediately freeze tokens during an exploit? Because it isn’t practical; it’s impossibly hard for stablecoin issuers to monitor every protocol, and it puts them on a slippery slope of deciding whether to honor the rights of protocols or holders in accordance with the law. In the case of the Drift protocol exploit it was a clear hack, but what about when it isn’t so clear? Issuing your own stablecoin gives the protocol full control and judgement and can dramatically reduce losses.

However, we also need to evolve the paradigm. In reality, protocols can never be built 100% secure, and institutions need to hedge their risk.

TradFi already manages counterparty and credit risk through credit default swaps and insurance. A similar opportunity exists on-chain: protocols could allow depositors to purchase insurance or credit default swaps to protect against losses. One promising approach uses prediction markets, where participants can take the long side (buying protection) or the short side (collecting premiums by betting on protocol safety). These markets would not only provide hedging tools but also create real-time transparency on which platforms are viewed as most creditworthy.

We’re overdue for a Security Renaissance which involves Protocols taking greater control, delivering greater transparency, and market-forces so that large depositors can ‘buy their own security’.

2/ Institutional Grade Buy-Side Tooling

Consider an institutional allocator seeking to deploy $100 million into tokenized assets. They would reasonably ask: What platform exists today that allows me to discover opportunities with full prospectuses, invest and custody across chains, protect against MEV and liquidation risk, monitor portfolio performance, and efficiently loop positions?

The honest answer is that no such institutional-grade platform yet exists. We have built a rich set of tokenized assets — from treasuries to equities — but we have not yet built the serious infrastructure required to deploy and manage institutional capital at scale.

Now is the time to start building the tooling institutional buyers need. There are a few major gaps I see.

The first is institutional-grade UIs that provide the holistic capabilities discussed above. Investing onchain is much more complicated than in TradFi and investors need solutions that provide them the requisite risk profiles and help with cross-chain custody and execution. One investor recently bought $50m of AAVE through the official Aave site and walked away with $36k worth of real tokens [link]. That’s the user experience institutional capital faces today. It would make sure that investors are protected against front-running and other MEV-related exploits.

Another key feature would be short-term liquidation insurance or protection. Most oracles are robust but not perfect. Institutions cannot be liquidated over a short-term oracle issue or other unrelated contagion that negatively affects their asset’s perceived price. I envision there would be a variety of crypto-native market makers who’d gladly take the other side in temporary market mispricings. Individual protocols offer this today, but institutions would want a more universal approach.

A final element for a platform could be 1-click looping. Platforms like Pendle and Kamino enable looping a prescribed list of assets. But managers may want to loop assets not offered on those platforms. There’s a clear protocol opportunity to publish a set of looping contracts that can be made accessible in the UI of wallets and institutional-grade platforms for any asset.

3/ Ability to Trade in Size

The last frontier is privacy.

Liquidity used to be the bottleneck. PropAMMs largely solved that, enabling low-latency dynamic quoting that drives capital efficiency and superior liquidity while reducing bad MEV compared to static AMMs.

But liquidity isn’t the only thing institutions need. Trade intents are still public, trading algorithms can still be reverse-engineered, and funds are still required for settlement within the block. Institutions can’t scale out of pilot mode if every position, hedge, and execution is visible in real time — and they won’t. This is why Canton, a blockchain optimized for TradFi confidentiality, has reached a multi-billion dollar valuation. It’s also why some whales avoid Hyperliquid despite its depth: placing orders moves the market against them.

The unlock is shielded execution against public liquidity. Silhouette [link] — a Hyperliquid shielded trading product — offers exactly this through a TEE-powered matching engine. Orders are batched, crossed, and netted privately without leaking intent; any unfilled portion routes directly to HyperCore’s public orderbook. Spot is live today, and has generated blended savings of 4bps per trade due to netting. Perps launch this year.

OTC desks and centralized exchanges will continue to fill large trades. But the full benefits of onchain finance at scale — instant settlement, reduced counterparty risk, deeper unified liquidity — only materialize when execution itself can be shielded.

Conclusion

The first $350bn came mostly from stablecoins.

The next order of magnitude is harder. It requires winning capital that has every reason to stay in TradFi: capital that cares about counterparty risk more than throughput, strategy confidentiality more than composability, and institutional-grade tooling more than ideology.

Capital won’t move onchain because tokenization is novel. It will move when tokenization delivers a structurally better risk-adjusted return. The Tokenization Premium points to high-value assets, the three gaps the problems to solve.

Tokenizing trillions is no longer a question of if. It is a question of who will build the applications in which these assets are issued, traded, and custodied at global scale.

We believe the opportunity is real and arriving. If you are building in this space, we would love to connect.